Skip to main content

Blog

VIDEO

ORIGINALS

SUBSCRIBE

TESTIMONIALS

DONATE

Theme:

Follow Us

Subscribe

Donate

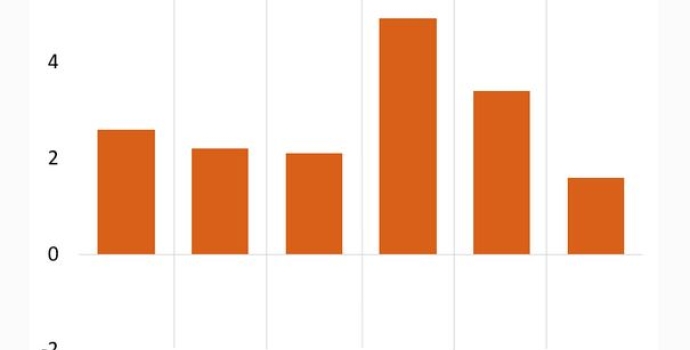

GDP Suffers Lowest Growth Since Second Quarter of 2022

Craig Bannister

All 10 Worst States for Business Run by Dems, 8 of 10 Best Led by GOP, CEO Survey Shows

Craig Bannister

Levin Posts ‘Once Upon a Time’ Video of ’60 Minutes’ Actually Doing Its Job, Grilling Pelosi

Craig Bannister

UCLA DEI Official Plagiarized Dissertation, Report Reveals

Evan Poellinger

Video

Rep. Ocasio-Cortez Thanks RNC for Posting Video of Her Praising ‘Peaceful’ Campus Rioters

Craig Bannister

Latest

Democrats Have Trump Right Where They Want Him, Trump Attorney Says

Craig Bannister

Planet Fitness Doubles Down on DEI With New CEO

Evan Poellinger

Anti-Israel Activists Vandalize Congressman’s Office

Craig Bannister

The Sex of Angels

Charles A. Kohlhaas

Papua New Guinea PM Bites Back at Biden Over Cannibal Claim

Craig Bannister

UT Austin Students Protest Dissolution of DEI Positions and Firings

Craig Bannister

$6 Billion a Day

Charles A. Kohlhaas

Unanimous Supreme Court Opens Door to More Anti-DEI Lawsuits

Evan Poellinger

These 14 Reps. Voted Against Resolution Supporting Israel’s Retaliation, Including All of ‘The Squad,’ 1 Republican

Craig Bannister

Pagination

Current page

1

Page

2

Page

3

Page

4

Page

5

Page

6

Page

7

Page

8

Page

9

…

Next page

›

Last page

››

Read More

Subscribe to Our Newsletter!

Click Here